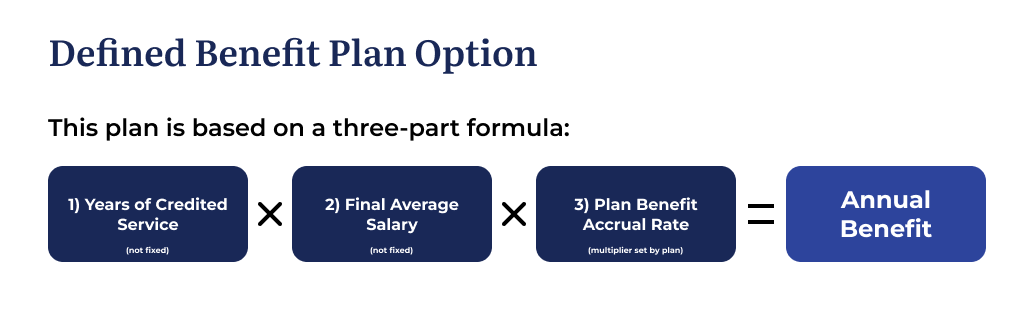

Flowchart detailing the calculation for a Defined Benefit Plan Option. The Annual Benefit is calculated using a three-part formula: 1) Years of Credited Service multiplied by 2) Final Average Salary multiplied by 3) Plan Benefit Accrual Rate equals Annual Benefit.

Defined Benefit plans are considered “traditional pension” plans. Employee retirement payments are based on a pre-set formula and takes into account:

- Years of credited service

- Final average salary

- The plan benefit accrual rate (multiplier) determined by the employer

For Example: 10 (years of credited service) x $30,000 (final average salary) x .05 (accrual rate/multiplier) = $15,000 (annual pension benefit).

Employers who place a high value on retaining employees for long periods of time have often elected to utilize a DB plan.

Employees who desire long term employment stability are attracted by a DB retirement plan that allow them to orderly plan for their retirement. When employees recognize the overall value of a DB plan offered by their employer and when employers can recognize that a DB plan will help facilitate tangible economic growth with highly satisfied and highly dedicated employees, a DB plan can be a sustainable and cost-effective benefit supported by both parties. Employees may be required to make contributions to assist with funding their retirement benefit (decided by employer’s board).

How is a defined benefit plan funded?

- Employer contributions

- Employee contributions

- Earnings on investments